Olena Ruban/Moment via Getty Images

Cannabis stocks have been hot. Even amidst a strong start to stocks overall, the AdvisorShares Pure US Cannabis ETF (NYSEARCA:MSOS) is up around 50% year to date, which I remind is just around one month’s time. After peaking at above $50 per share in 2021, MSOS dropped 90% over the next two years. The sector looked all but forgotten but has seen a spark of new life amidst hopes that the Drug Enforce Administration (‘DEA’) might reschedule cannabis to Schedule III, which would lower cannabis corporate tax rates and dramatically boost cash flows. While the rally may be taking a bit of a breather as of late as a government official dismissed rumors of an imminent rescheduling, the sector remains red-hot with a highly visible near term catalyst. MSOS is an ideal way to invest in this latest cannabis hype cycle though I detail the risks and reservations.

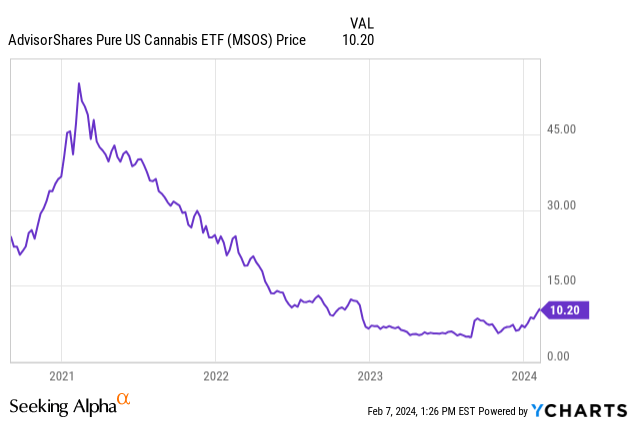

MSOS Stock ETF Price

MSOS was once on top of the world, as investors hoped for a swift decriminalization of cannabis following the 2020 elections. Those hopes proved too optimistic, and cannabis companies saw growth rates struggle following the pandemic boom. What followed was a swift re-rating downwards.

While the long term picture remains ugly, MSOS is up 100% over the last three months alone.

Why MSOS?

MSOS is an NYSE-traded ETF that owns the stocks of the cannabis multi-state operators (hence its ticker). With cannabis being illegal on the federal level, US cannabis stocks are unable to trade on the major exchanges and instead trade on the over-the-counter pink sheets. MSOS is able to avoid such treatment due to the fact that it does not own its underlying stocks directly, as it instead owns “total return swaps.” This clever solution has enabled it to offer investors a convenient and highly liquid way to invest in a broad basket of US cannabis stocks.

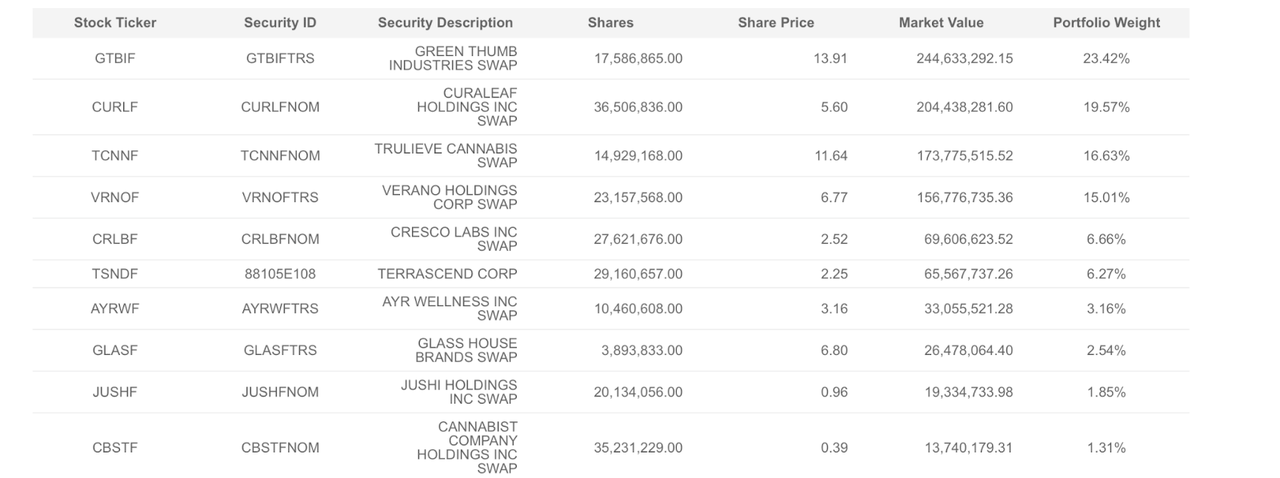

MSOS ETF Stock Holdings

The MSOS, as its name suggests, owns the stock of the multi-state operators, including the largest names like Green Thumb Industries (OTCQX:GTBIF), Curaleaf (OTCPK:CURLF), Trulieve (OTCQX:TCNNF), and Verano (OTCQX:VRNOF). The fund owns some single-state operators (‘SSOs’) like Glass House Brands (OTC:GLASF) but nowadays the majority of publicly traded US cannabis stocks operate in multiple jurisdictions.

MSOS

The fund has heavy concentration in the top-6 holdings, making up 87.5% of the portfolio value, but this is not a concern of mine given that the largest operators do deserve greater allocation given that the fund appears to be attempting to offer somewhat passive sector-exposure. I note that this is technically an actively managed fund and it carries a 0.83% expense ratio.

Is MSOS Stock ETF A Buy, Sell, Or Hold?

Historically, many investors have invested in the stocks of the Canadian operators like Canopy Growth (CGC) or Tilray (TLRY) to express a bullish view on US cannabis. That view made some sense, as these companies own large greenhouses that could ramp up production if allowed to export into the country. However, it is clear that we are still many years, if not at least a decade away from the full legalization needed to allow international imports. I do not expect a successful rescheduling to yield any financial benefit for Canadian cannabis operators. Instead, it is the US cannabis operators that stand to benefit drastically. Consider the stock of VRNOF, one of my favorite operators in the sector. The company generated $27 million in taxable income in the latest quarter, but recorded $45 million in income tax provisions. That led the company to post a GAAP net loss. If cannabis were rescheduled to Schedule III, then these “280e taxes” should disappear and VRNOF might instead pay a more normalized 21% tax rate, leading to $21 million in positive GAAP net income. The company would go from negative GAAP profitability to trading at around 29x GAAP earnings. These companies would suddenly improve in credit quality which would help them refinance maturing debt at more favorable rates. The impact can not be understated.

I must emphasize caution, however. Glancing at the valuations for some of the top operators, it is not immediately obvious that the names are that cheap. I have included a smaller operator in Ascend Wellness (OTCQX:AAWH) as well.

Cannabis Growth Portfolio

I view GTBIF to be the top operator in the sector due to it sustaining positive GAAP net income even under the current regulatory environment. Yet at 11x adjusted EBITDA, it isn’t immediately obvious that this is “dirt cheap.” Perhaps one could see an argument for the stock to re-rate to 15x adjusted EBITDA upon rescheduling, but it is difficult to call for more or a sustained premium given the price compression headwinds facing the sector. For this reason, some investors might prefer to invest in individual names like AAWH which trade at lower valuation multiples, as the smaller operators tend to make up a smaller component of the MSOS ETF. Yet here it also isn’t so simple. I expect the smaller operators to continue to trade at a relative discount to the larger operators, thus if the larger operators have moderated upside then that may extend to the smaller operators as well. On the flip side, if rescheduling were to not occur, then it is possible if not likely that cannabis stocks reverse course and resume a downward slide, as these companies would have to deal with refinancing maturing debt in this higher interest rate environment. Furthermore, given the hype-driven nature of this investment, it is difficult to know which stocks might offer the greatest upside in any rally. Due to MSOS offering the most convenient liquidity, it stands to reason that the fund offers the most realistic chances of getting optimal exposure to the upside.

Closing Thoughts

Cannabis stocks appear to be offering their most promising setups in years with rescheduling being a real near term catalyst. The last several years of financial struggles has dampened my enthusiasm for long term valuations, as well as my ability to suggest any sort of conviction as of present day. However, MSOS may be an appealing investment choice for those looking to express a bullish near term or long term view for US cannabis. I continue to prefer investing via the cannabis REIT NewLake Capital Partners (OTCQX:NLCP), which is a landlord to many of the names held in MSOS but trades at a near 10% dividend yield with no net debt on its balance sheet. Even so, I can see an argument for owning some exposure to MSOS given the catalyst-driven setup.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.